|

This

course is for the expert user who

has good experience with Microsoft Excel or has completed the five

courses in our

Beginner Series plus Expert Level 1,

2,

3,

4 and

5 classes. This course will teach you how to work with

financial functions in Excel.

We will

begin by learning about Excel's financial terms and functions including

PV (present value), FV (future value), PMT

(payment), RATE (interest rate), and NPER (number of

periods). You will learn about APR (annual percentage rate) and

simple vs. compound interest.

Next you'll build a loan calculator

where you will use the PMT function to determine the monthly

payment for a loan (home mortgage, car loan, etc.) knowing the value of

the loan, interest rate, and term of the loan (years). We will be able

to examine multiple scenarios by adjusting the variables to determine

the best loan for our needs.

In the next lesson, we'll build an

investment calculator. If you deposit money into an account and have

a set APR, we'll calculate how much money you'll have in your account

after so many years. We'll use the FV (future value) function for

this.

Next we'll build an interest rate

calculator. If you know your initial deposit and the current value

of the investment, you can use the RATE function to calculate

your return on investment.

Next comes a fun project I like to call

the millionaire calculator. You can use this to determine how

long until you become a millionaire. Or, if you only want to save, say,

$500k for retirement, this spreadsheet will tell you how long it will

take. You input the initial deposit amount, the amount you're going to

pay into the account every month, your goal amount, and the interest

rate. The NPER function will tell you the number of periods

(months or years) until your goal is met. This is great for calculating

the time until you can retire.

Next comes the initial deposit

calculator. Knowing the current balance of an account, the interest

rate, and how long the account has been open, you can calculate what the

initial deposit was using the PV function.

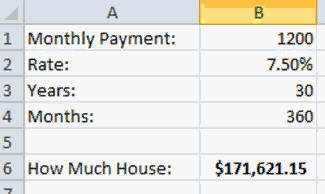

Along the same lines, you can also use

the PV function to calculate how much house you can afford when

you go home shopping. If you know what monthly payment you can

afford, what your interest rate is going to be, and how many years you

want a mortgage for, the PV function can tell you how much house

you can afford to buy.

Next we'll learn how to build a loan

amortization schedule. We'll look at one of Microsoft's templates to

see a good example, and then we'll actually build our own so you

understand all of the functions involved. You'll learn about the IPMT

and PPMT functions which can calculate how much of a monthly

payment is interest and principal, respectively. You'll also use the

CUMPRINC and CUMIPMT functions to calculate interest and

principal between any two points in the loan.

Finally, we'll take a look at your

credit card statement. We'll use the NPER function to

determine how long it will take to pay off your credit card debt if you

just make the monthly minimum payments. Then, we'll use the

PMT function figure out how much you'll have to pay every month if

you want to pay off your debt in, say, 6 months, a year, or 3 years.

You'll see how much the credit card companies are REALLY making

off of you!

Again, this is the perfect class

for anyone who wants to learn how to work effectively with financial

functions in Microsoft Excel

. Of

course, if you have any questions about whether or not this class is

for you, please contact me.

Complete Outline - Excel

Expert Level 6

00. Intro (6:14)

01. Financial Terms (4:49)

PV, FV, PMT, RATE, NPER

APR (Annual Percentage Rate)

Simple Interest

Compound Interest

02. Loan Calculator (9:39)

Calculate Mortgage Payment

PMT function

Compare Multiple Scenarios

03. Investment Calculator (5:03)

FV Future Value Function

Calculate Investment in 5 Years

04. Interest Rate Calculator (6:09)

What is your Return on Investment

RATE function

Calculate interest rate

05. Millionaire Calculator (6:01)

NPER Function

How many years until goal reached |

06. Initial Deposit Calculator (2:29)

PV Function

What was the initial deposit?

07. Home Value Calculator (4:04)

How much house can I afford

PV function

Optional FV and TYPE parameters

08. Loan Amortization (12:10)

Microsoft's Amortization Template

Create your own amortization table

IPMT, PPMT functions

Cumulative interest and principal paid

CUMPRINC, CUMIPMT

09. Credit Card Payments (6:08)

How many payments at minimum

How long to pay off card debt

What payment to pay off in 6 months?

NPER and PMT

10. Review (4:44) |

|

| Keywords:

microsoft excel tutorial, microsoft excel tutorial, microsoft office excel tutorial, microsoft excel training, financial, PV, FV, PMT, RATE, NPER, APR, simple, compound interest, loan, calculator, investment, interest rate, ROI, return on investment, millionaire, initial deposit, home value, TYPE, amortization, IPMT, PPMT, CUMPRINC, CUMIPMT, cumulative, principal, credit card, payoff |